Speculation on the future of interest rate policy and market movements is a hot topic at the moment – both in the media and within financial circles.

We at Natgen have been watching these developments closely, given the fact that we have been following our interest rate risk management strategy for some time now.

The basic tenets of our strategy are as follows:

The assumption is that the next interest rate movements will be upwards.

Governments and the banking/finance communities worldwide have a vested interest in keeping interest rate movements within a tolerable band for mortgage holders in particular.

Our base case assumes a doubling of effective interest rates within the next interest rate cycle, meaning in increase over the coming years of approximately 2% per annum.

The speed of interest rate increases is unable to be accurately determined, so we use the market rates for BBSY between 90 days and 10 years as an indication of the market view of the expected rate of rise in interest rates.

Our financial models for Natgen investment trusts assume a commencing interest rate above the current short term BBSY (bank bill swap rate) and provide an increase in this rate during the latter years of Natgen investment trusts based on advice from financiers, other market participants and Reserve Bank guidance.

The response to this interest rate information may vary. For example, Natgen has chosen to fix the interest rate of the debt for the Kingsthorpe Central Shopping Centre for the term of the loan, whereas the interest rate for Rededge Goodna will remain variable in the short term, pending further market indications. Both these responses are based on our interpretation of available information and our consideration of the best outcomes for our unitholders in each individual case.

Current interest rate market indications

Following the most recent inflation figures, medium term fixed interest rates jumped significantly, indicating that the market is factoring in a series of increases earlier than previously expected.

The consensus view of bank economists is bringing interest rates increases forward from 2024 into 2023 and to some extent into the latter part of 2022. The Reserve Bank, on the other hand, is taking a somewhat more conservative approach. In its latest Statement on Monetary Policy (November 2021), the Reserve Bank has made observations about the international environment, domestic economic conditions and domestic financial conditions which are consistent with it’s conservative growth expectations on interest rates.Whilst a multitude of factors are at play, my reading is that the RBA sees the current inflation spike as just that – a spike, which has been caused largely by supply constraints as global supply chains re-start following Covid-related shutdowns on all continents. The Delta strain further extended supply constraint conditions. However, as supply chains recover, the expectation is that the inflation spike will normalise and long term inflationary pressures will return to closer to pre-pandemic levels. Even widely-publicised labour market shortages are expected to have only moderate impacts in Australia, given our predominantly services based economy and reintroduction of foreign students and workers into the economy in 2022.In the end, only time will tell whether the market response or RBA analysis is correct. Notwithstanding this uncertainty, we at Natgen will continue to take a risk-managed approach to interest rate decision making, with unitholder return and risk reduction as the central considerations.Steven Goakes

Managing Director For 2022 Natgen opportunities, please visit: https://natgen.com.au/investment-opportunity

Natgen provides clients with well-considered, carefully measured commercial investment opportunities, accompanied by professional advice from our experienced leaders.

If you’d like to be notified of future investment opportunities, request an Investor Information Pack or contact us directly at invest@natgen.com.au

As the end of the financial year approached, I spent some time looking back at the position of the world and this country at the beginning of the financial year. On 1 July 2020, the following was happening:

The first wave COVID-19 disasters had swamped the UK, USA, Italy and many other countries;

Fortress Australia was in place and our first wave had been controlled;

A COVID-19 vaccine seemed a distant hope – perhaps for 2022 or 2023;

The ASX was stuttering back after a March rout;

Close to 3.5 million Australians were being supported by Jobkeeper, following the loss of somewhere between 1 and 2 million jobs;

Property markets were flat;

All Australian governments were putting on a united front (remember that!); and

There was significant pessimism about near-term economic performance of the economy.

We were yet to face devastating second and third waves of the pandemic globally and the scary spectre of the removal of Jobkeeper support after September.

As astonishing as the pandemic was in its impact and consequences, the ‘snap back’ has been equally astonishing, with significant winners and losers along the way.

My hope for this coming year is that short-term survival behaviour gives way to long-term strategy and vision, both for individuals, corporations and countries. Whilst they may appear at times to have been suspended, the fundamentals of economics, politics and the social contract have not gone away. We best recognise this sooner rather than later.

2021-2022 Financial Year: What’s next?

Since completing our latest investment trust Natgen Investment Trust KT21 at the beginning of May this year (only 2 months ago), we have been fielding constant queries about when and what is next for Natgen and it’s investors.

The constant (and truthful) response is that we are diligently seeking new opportunities for our investors which accord to the immutable principles of the Natgen Investment Philosophy.

Markets are hot right now – some might say behaving irrationally. Experience tells us that value remains available in these times, but one must seek it out in a careful, sober and meticulous manner. It is a time where we get to demonstrate our values, for whilst it would be better for us (as a company) to take on as many new transactions as possible, this would not be in the best interests of our investors, who rely on us to provide thought leadership in terms of where value and growth can be found. Our long term survival and prosperity will come from demonstrating that we live our values and continue to put investor’s interests first. After all, this is the fundamental tenet of a fiduciary relationship – always has been, always will be.

Don’t worry – when we find value passing a transaction through our due diligence processes, you will be informed and be invited to participate. In every case, we ask you to challenge us to explain to you our underlying value proposition for the transaction. Our philosophy and processes ensure that we will have a good answer to that question.

Interest rates and their future impacts

The low interest rate environment that we currently enjoy has presented threats and opportunities across the economy. In particular, it has impacted prices of residential property substantially and commercial property also, but to a lesser extent.

But interest rates will not stay stagnant forever, and logic suggests that the next movements will be up. Thus, we are constantly focussing on interest rate risk management in all transactions we are considering. It is not sufficient to predict that rates will remain where they are for term of a trust. We at Natgen are seeking regular (at least monthly and often weekly) briefings from our preferred debt providers and adjusting our interest rate considerations accordingly.

Ultimately, no-one actually knows where or when rate movements will occur. What we can do, however, is take a well-informed, risk-managed position on interest rates and manage our portfolio and future transactions accordingly.

I wish you well for the year ahead.

Regards

Steven Goakes

Natgen provides clients with well-considered, carefully measured commercial investment opportunities, accompanied by professional advice from our experienced leaders.

If you’d like to be notified of future investment opportunities, request an Investor Information Pack or contact us directly at invest@natgen.com.au

Many of our investors invest in Natgen Trusts via their self-managed super funds (SMSF).

Natgen Trusts acquire commercial property assets, and investors (including SMSFs) participate in our trusts to access commercial real estate assets for enhanced diversification and returns in their investment portfolios. This allows them to benefit from commercial property assets without the burden of managing them directly.Being able to invest in commercial property in your SMSF is of course dependent on a number of factors, and it is always best to check with your accountant or adviser as to your own personal situation.

How much should my SMSF invest?

Typically, SMSF’s will have an investment strategy which will act like a road map for the fund’s trustees when they decide on investments. It is there to help the fund meet its sole purpose of providing members with a retirement benefit or to their dependents should a member die before retirement.

The investment strategy may be as simple as having a certain percentage of the fund’s investment allocated to each asset class, or be more complicated and prescriptive. Ultimately, the strategy is as individual as the members of the fund and set out why and how to invest these funds to meet these goals.

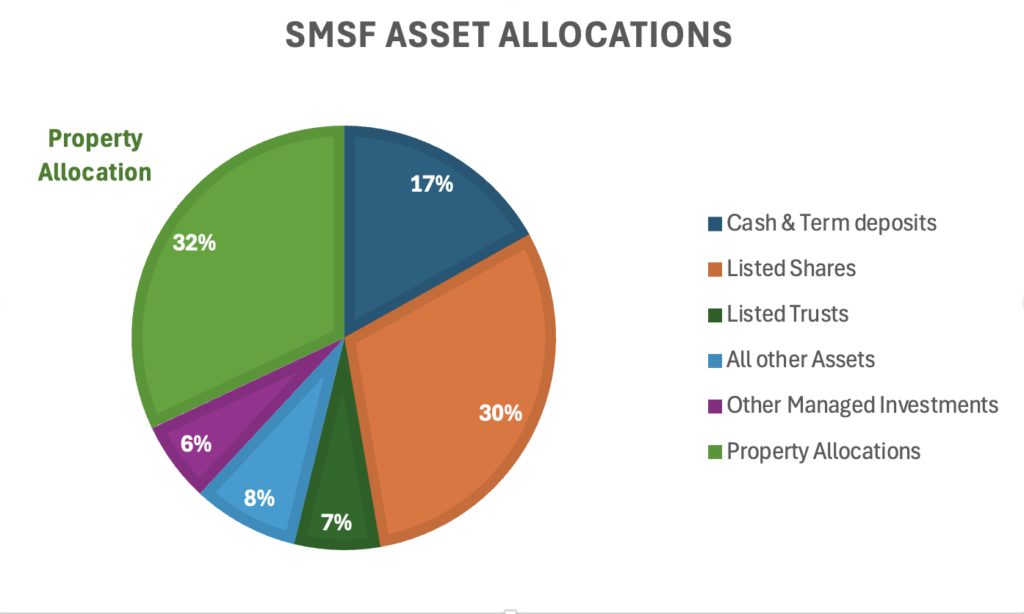

The Australian Tax Office (ATO) is the regulator for SMSFs and therefore have incredible oversight over how funds are run, and what assets they own. They published data[1] which shows that most SMSFs on average have anywhere between 20-32% allocation to property investments. This can be direct investment in residential real property, commercial real estate, limited recourse borrowing arrangements (LRBAs are specifically a structure to borrow to invest in property), or investment via unlisted trusts like the Natgen Investment Trusts.

Commercial property assets help bring diversification to investment portfolios, and it is through diversification of asset classes and investments that help reduce risks and achieve more stable returns in the long run.

More about SMSFs

Self Managed Superannuation Fund (SMSF) Origins

Did you know that the Australian pension system is the 5th largest in the world (behind the USA, UK, Japan, & Canada), and mandated to grow by more than 11.5% p.a? Not bad for a country with a population (just under the size of the city of Shanghai) of ~26.7million and with around ~$3.8 trillion in savings.

Australians have been providing for one another since 1909 with the introduction of the publicly funded Aged Pension in 1909. But it wasn’t until Prime Minister Paul Keating enacted the Superannuation Guarantee on July 1st, 1992 which saw employers[1] contribute 4% of their employees’ wage to their superannuation account.

Since then, Australia’s retirement income system has been viewed as a model for other nations with its 3 pillar approach of;

As our pension system evolved, it wasn’t until the Wallis Inquiry in 1999 which allowed small businesses and the self employed to establish and manage their own superannuation accounts – creating the very first SMSFs[3].

What is an SMSF?

A self-managed superannuation fund (SMSF) is a private fund that you can manage yourself, as distinct from an industry or retail fund where those funds choose investment and insurance options for you. But having that level of control over your own fund also comes with a number of rules and responsibilities[4] to ensure your fund meets the sole purpose test of providing retirement benefits for members.

Investment Restrictions

The Superannuation Industry (Supervision) Act 1993 (SIS Act) is the legislation outlining the various rules trustees must follow when managing an SMSF.

SMSF investments must be made on an arm’s length basis; meaning that the purchase and sale price of fund assets should always reflect the true market value, as should income from the fund assets.

There are a number of rules outlined in the SIS Act to ensure a fund meets the sole purpose test. They affect how and what your fund can investment in such as;

Related Parties and Relatives

No one associated with your fund should get a present-day benefit from its investments.

Loans and Early Access

You can’t lend money or provide direct or indirect financial assistance from your fund to a member, or a member’s relative.

Acquiring Assets from Related Parties

SMSF trustee is prohibited from acquiring assets from trustees of the SMSF, their relatives or related entities (except for securities listed on a prescribed exchange and business real property).

In-House Assets

An in-house asset is a loan to, an investment in, or a lease of an asset to, a related party or entity of the SMSF.

Business and real property

Trustees need to ensure the level of investment in business real property still meets the investment strategy of the fund, including diversification of assets, liquidity and maximisation of member returns in the fund.

Collectible & Personal use assets

Investments in such items must be made for genuine retirement purposes, not to provide any present-day benefit. The ATO outlined how this works for jewellery, artwork and other assets.

Borrowing

Subject to specific exception, an SMSF trustee is prohibited from borrowing or maintaining an existing borrowing of money.

The table above highlights some of the concepts, but of course Trustees should consult with the ATO website and their professional advisers with how this relates to their situation.

Natgen provides clients with well-considered, carefully measured commercial investment opportunities, accompanied by professional advice from our experienced leaders.

If you’d like to be notified of future investment opportunities, request an Investor Information Pack or contact us directly at invest@natgen.com.au

Steven Goakes

Managing Director For 2022 Natgen opportunities, please visit: https://natgen.com.au/investment-opportunity

Steven Goakes

Managing Director For 2022 Natgen opportunities, please visit: https://natgen.com.au/investment-opportunity