South-East Queensland Growth Is No Accident - And Neither Is Our Focus

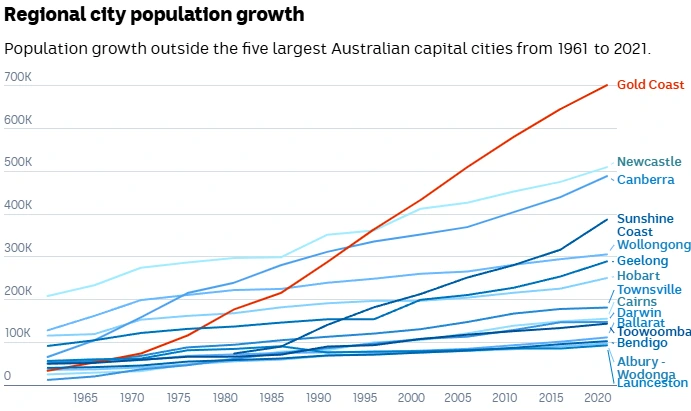

From its origins as a quiet little surf town in the 1960s, the Gold Coast has grown into Australia’s sixth largest city. That transformation has been driven by sustained population growth chasing lifestyle, related infrastructure investment, and a steadily expanding and diversified economic base.

As highlighted in a recent ABC News article, this growth is far from over. South-East Queensland is expected to continue absorbing significant population inflows over the coming decades, placing increasing demand not only on housing, but on the commercial property that supports it – from retail and services through to logistics, storage and workspace.

This is where Natgen identified an opportunity early.

As population growth accelerated on the Gold Coast through the late 2010s, Natgen’s development business recognised that new residents bring more than just demand for housing. They also drive demand for the “next layer” of property – the spaces where small businesses operate, trades are based, and equipment and goods are stored.

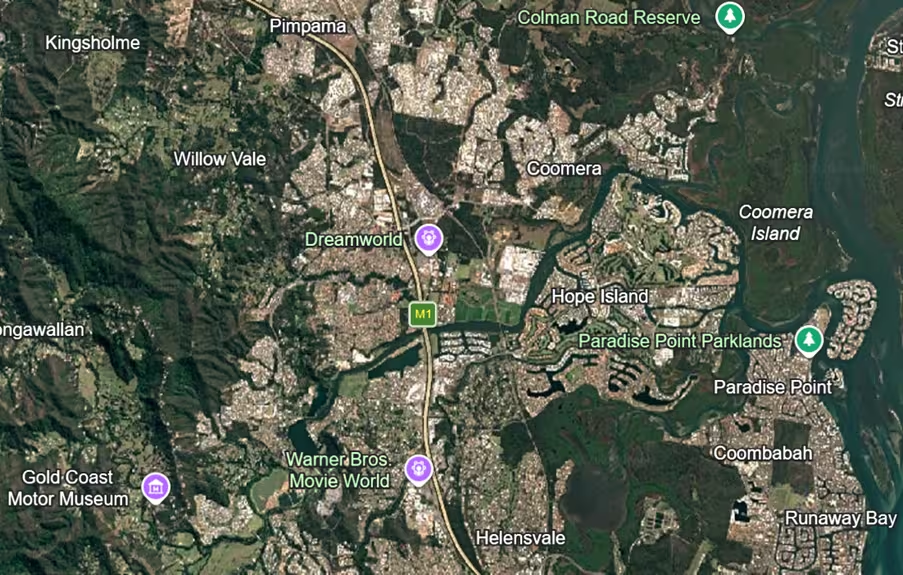

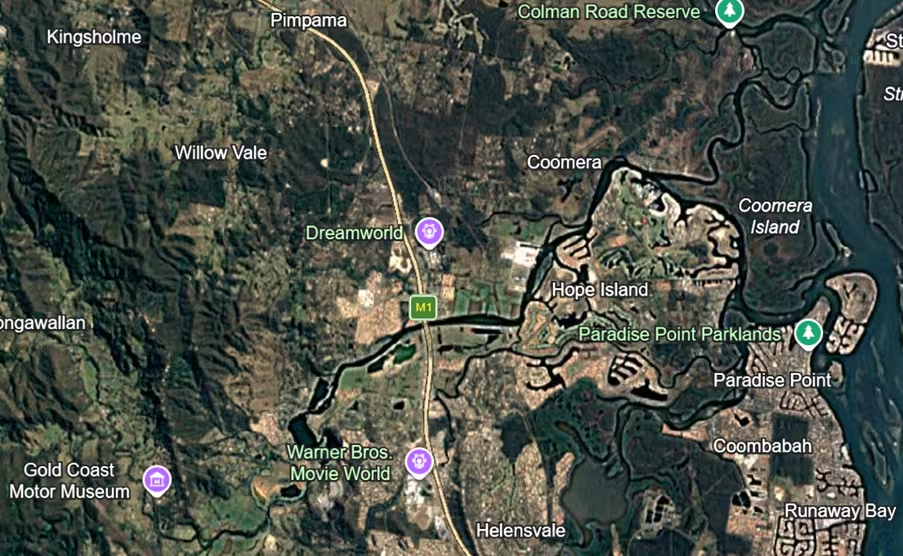

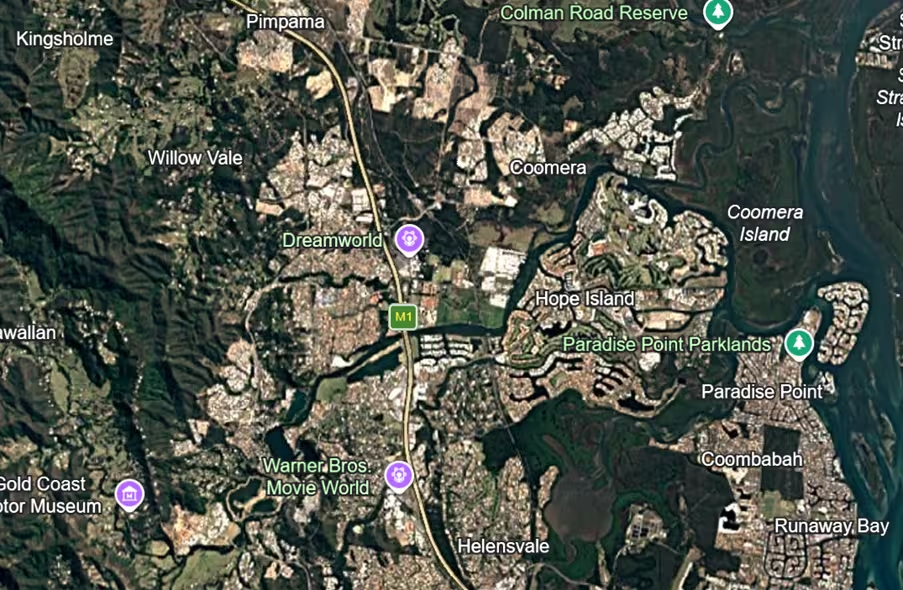

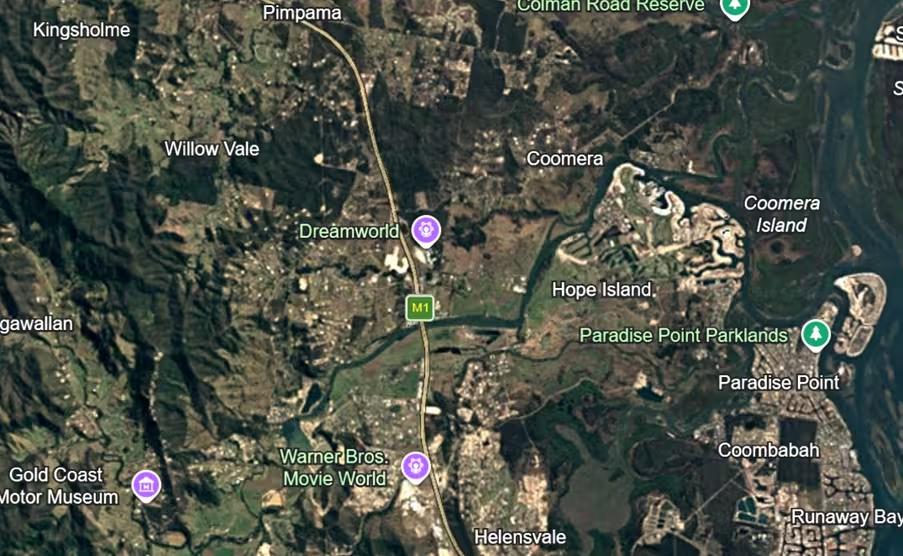

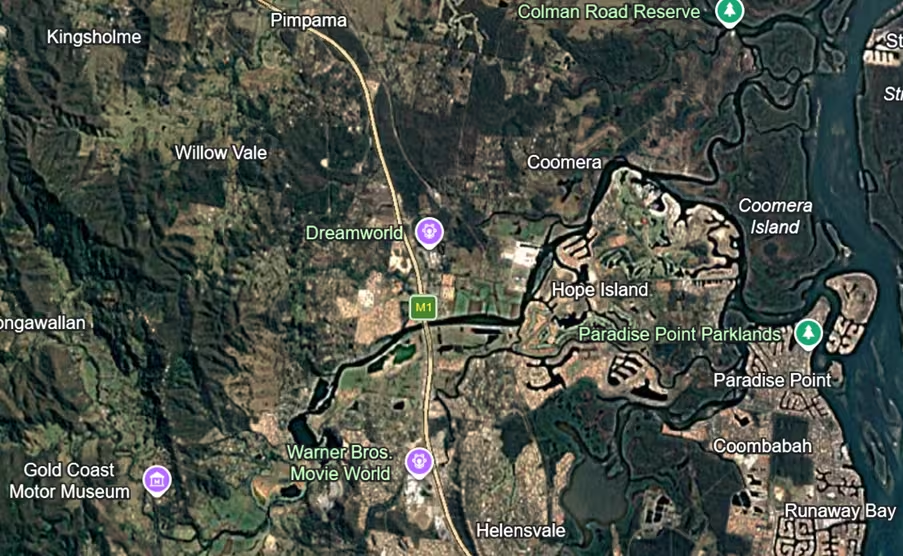

Since 2019, Natgen has focused on delivering strata office and warehouse developments across South-East Queensland, targeting established growth corridors along key infrastructure such as the M1 Motorway, particularly across the northern Gold Coast.

These developments are designed to cater for a broad and growing user base – from trade operators and small businesses through to residents requiring secure storage for vehicles, equipment and lifestyle assets such as caravans and boats. As housing becomes more dense, this demand continues to increase.

This approach has delivered strong outcomes for investors. Of the 8 Natgen development offers to date, 5 have been delivered, and a 6th is in the final stages of delivery, with Natgen investors benefiting from both development profits and strong underlying demand for the product.

So what underpins this strategy?

At its core is a disciplined and repeatable process.

Natgen focuses on identifying sites with strong proximity attributes – close to population growth, infrastructure and established amenity. This is supported by a detailed analysis and understanding of local supply and demand fundamentals, ensuring developments are aligned with real market need.

From there, the focus is simple: buy well, manage the development process well, and sell well.

Sites are typically secured off-market at prices supporting the feasibility of the projects. Projects are then actively managed with a strong emphasis on design optimisation, cost control, and disciplined delivery. Finally, assets are brought to market in a way that maximises value, supported by underlying demand from both owner-occupiers and investors.

While the broader growth story of South-East Queensland is well understood, Natgen’s approach is centred on how to translate that growth into tangible investment outcomes.

It is not simply about following population – it is about understanding what that population needs next, and delivering the property that supports it.

Natgen Development Trusts are only offered to existing Natgen investors.

If you’d like to be notified of future investment opportunities, request an Investor Information Pack or contact us directly at invest@natgen.com.au.